This article has been translated from English to Gen Z Slang.

Ayy, central banks were totally vibing this week, teaching all the currency stans a quick lesson on how changing policy vibes can send traders into a panic, low-key looking to fix their positions. 😜

The Federal Reserve's move on Wednesday with their rate cut was a full-on main character moment—not just because they shaved off a quarter-point, but 'cause Chair Powell's statement low-key blaming tariffs for inflation and calling it temporary had the dollar taking a nosedive until Friday, despite some Fed peeps trying to throw some hawkish shade. 🕶️

Meanwhile, the European Central Bank crew stirred the pot by hinting rates might have bottomed out, the Reserve Bank of Australia teased us about a possible February tightening, and the Swiss National Bank was like “nah fam” to negative rates, even though inflation was looking weak. Result? The Swiss franc popped off, while the yen was left struggling at the bottom, even with Bank of Japan ready to flex those interest rates, showing how fully priced vibes can mess with even the hawkish peeps. 🤷

Let's spill the tea on how each major currency surfed through this cray week and what was fueling the tea.

Table of Contents

| U.S. Dollar | Canadian Dollar |

| Euro | Australian Dollar |

| British Pound | New Zealand Dollar |

| Swiss Franc | Japanese Yen |

USD Pairs

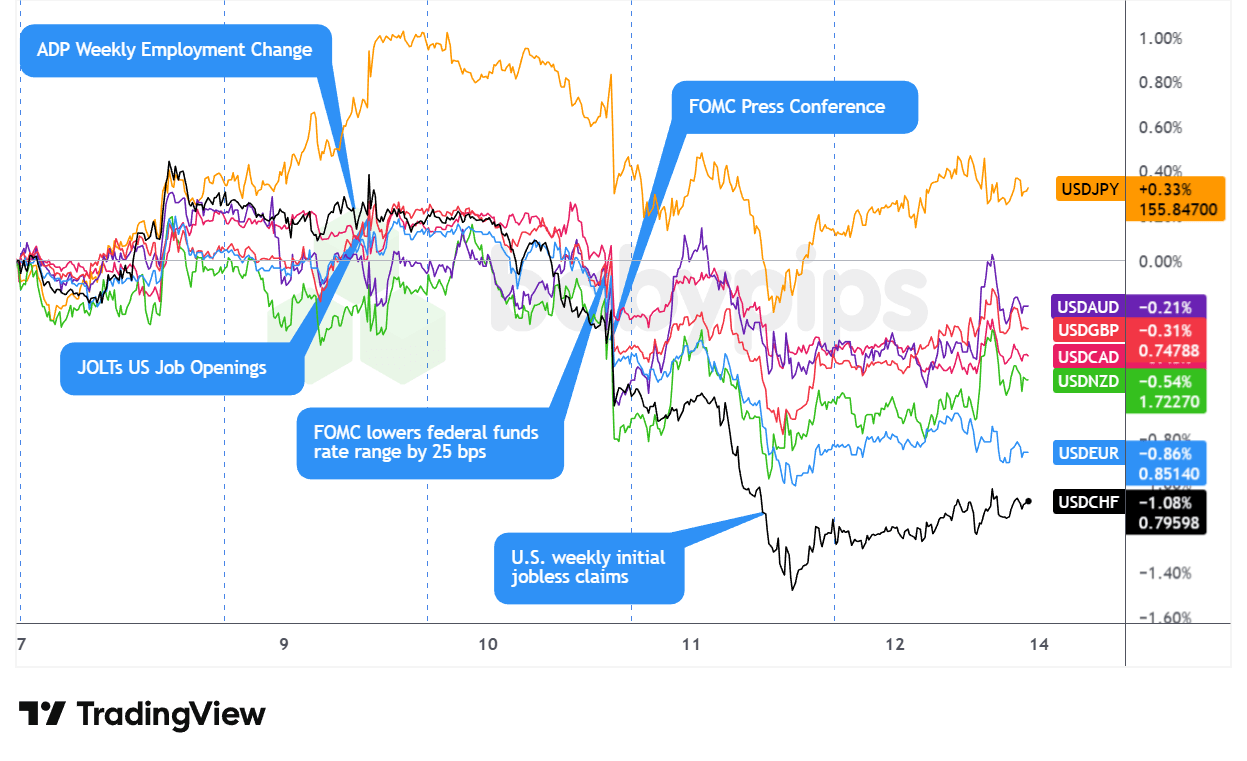

Overlay of USD vs. Major Currencies Chart by TradingView

The dollar kicked it strong at the start, shaking off weak Asian vibes to rally through Monday in Euro city. This strength appeared outta nowhere, meaning traders were probs gearing up for the Fed action, with the greenback getting comfy alongside low-key sketchy vibes and rising bonds. 📈

But Tuesday was kinda sus. The dollar was all over the place, hyped by stronger JOLTS data before kinda fizzling. Then, WHAM, Fed dropped its expected quarter-point cut Wednesday arvo. But the real shade came when Chair Powell’s dove-like take had the greenback seeing red. Talking about inflation as just an “oops, tariffs!" and predicting it will chill next year totally tanked the hawks' game, even if the FOMC was a bit split. 🤔

Our fave green hero took more Ls on Thursday, totally crashing through the Asian and London vibes despite some overnight tech bounce inspiration. The Swiss Bank’s predictable 0% stance was no help, with USD/CHF dropping 0.73% as everyone jumped ship. Then wham-bam, more shakens when weekly jobless claims shot up, reinforcing Powell’s warning about mad labor market drama, fueling thoughts of more rate cuts in 2026 beyond the Fed's initial plan. 🚀

Friday was kinda chill, as the dollar shook off the Thursday blues with some hawkish Fed vibes. Cleveland’s Hammack was all about “tighter feels” for rates, while dissenter Schmid doubled down on inflation worries. 🔥 Thirty-year yields hit some highs, pumping up the mood. But, LOL, the damage was done—the dollar dipped hard in the weekly charts despite Friday’s comeback tour. 🎤

Bullish Headline Arguments

- U.S. Consumer Inflation Expectations for November 2025: 3.2% (3.1% forecast; 3.2% previous)

-

FOMC Delivered 0.25% “Hawkish Cut” in Historic 9-3 Vote

- On Wednesday, the FOMC voted 9-3 to lower the benchmark federal funds rate by a quarter point to a range of 3.5%-3.75%

- The Summary of Economic Projections (SEP) for 2025 signaled only one rate cut in 2026, inline with September’s projections

- U.S. NFIB Business Optimism Index for November 2025: 99.0 (98.0 forecast; 98.2 previous)

- U.S. ADP Employment Change Weekly for November 22, 2025: 4.75k (-13.5k previous)

-

U.S. JOLTs Job Openings for October 2025: 7.67M (7.0M forecast; 7.66M previous)

- U.S. JOLTs Job Quits for October 2025: 2.94M (3.1M forecast; 3.13M previous)

- U.S. MBA 30-Year Mortgage Rate for December 5, 2025: 6.33% (6.32% previous)

- U.S. MBA Mortgage Applications for December 5, 2025: 4.8% (-1.4% previous)

-

U.S. Balance of Trade for September 2025: -52.8B (-57.0B forecast; -59.6B previous)

- U.S. Exports for September 2025: 289.3B (281.0B forecast; 280.8B previous)

- U.S. Wholesale Inventories for September 2025: 0.5% m/m (-0.3% m/m forecast; 0.0% m/m previous)

- Beth Hammack, Cleveland Fed president, argued on Friday that inflation is still too high and policy should be “a little” or “slightly” more restrictive than it is now

Bearish Headline Arguments

- U.S. officials hinted at future Fed rate cuts

- US White House adviser and Fed Chairperson contender Hassett said they should “continue to get the rate down some” with an eye on data

- On Tuesday, Kevin Hassett said there is “plenty of room” for the Fed to cut rates, potentially by more than 25 basis points, given what he sees as an AI-driven, 1990s-style productivity boom that can support lower rates without stoking inflation.

- Trump tells Politico he may consider changes to tariffs to lower prices; calls willingness to lower rates a “litmus test” for Fed chair choice

- U.S. Bureau of Labor Statistics will publish the October and November PPI data together in January

- U.S. Initial Jobless Claims for December 6, 2025: 236.0k (205.0k forecast; 191.0k previous)

- Fed says it will start technical buying of Treasury bills to manage market liquidity

- US President Trump doesn’t rule out troops in Venezuela, says President Nicolás Maduro’s ‘days are numbered’

- US President Trump threatened Mexico with 5% tariff increase over water dispute

-

U.S. Employment Cost – Wages QoQ for Q3 2025: 0.8% (0.8% forecast; 1.0% previous)

- U.S. Employment Cost Index QoQ for Q3 2025: 0.8% (0.8% forecast; 0.9% previous)

- U.S. Employment Cost – Benefits QoQ for Q3 2025: 0.8% (0.6% forecast; 0.7% previous)

- U.S. Imports for September 2025: 342.1B (338.0B forecast; 340.4B previous)

- Despite dissenting on a rate cut this past week, Federal Reserve Bank of Chicago President Goolsbee said he projects more interest rate cuts in 2026

EUR Pairs

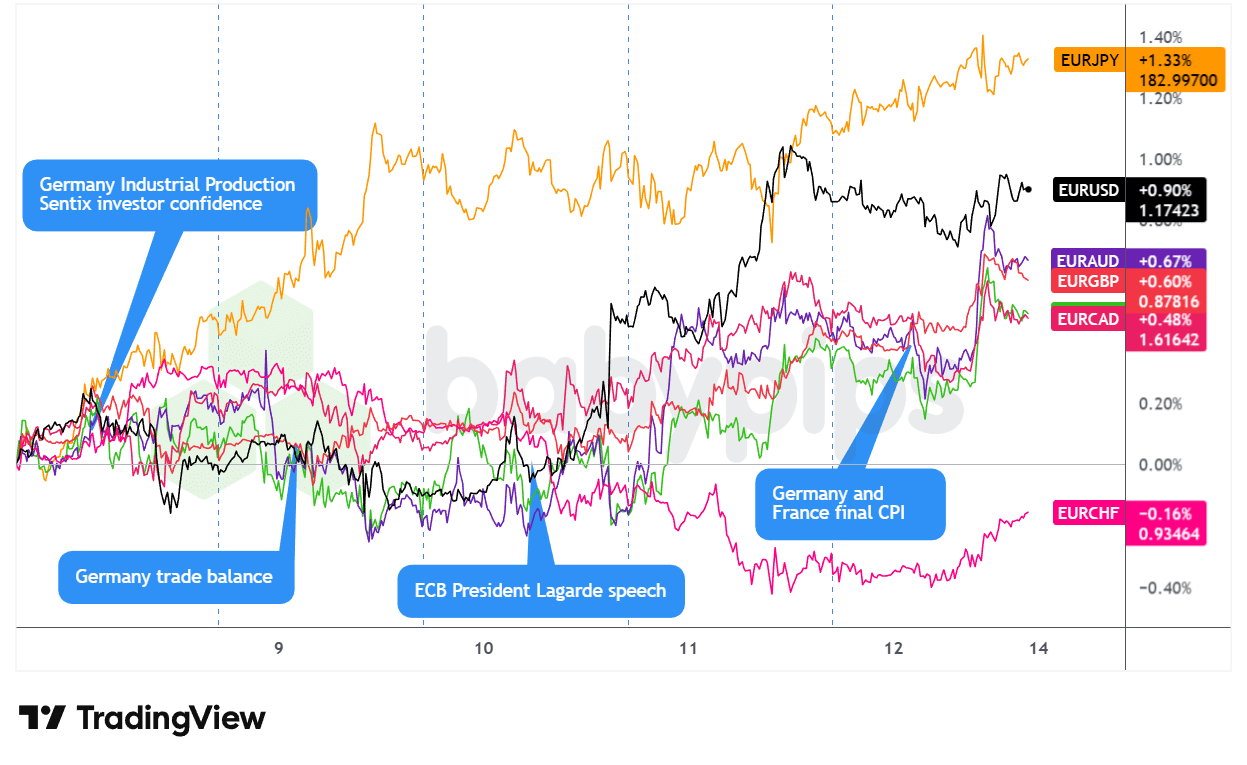

Overlay of EUR vs. Major Currencies Chart by TradingView

The euro was kinda meh for a while before popping off thanks to dovish Fed vibes and rising euro-centric feels with the ECB. 😎

Through Wednesday’s U.S. session, EUR was just chilling without much movement, even with Monday’s surprisingly strong German industrial prod (1.8% vs 0.4% guess) and Tuesday’s solid trade stats not really doing much. But TBH, nothing hit until the central banks started dropping hints. 🔉

The mood changed during the London sesh on Wednesday as ECB peeps Simkus and Villeroy hinted rates might stay at their chill levels, and Prez Lagarde thought December growth might even get an upgrade. This hawkish move on their end helped the euro stay upright until the U.S. crew clocked in—Powell’s characterization of tariff-driven inflation as temporary flipped the whole game, causing the dollar to sweat while lifting EUR/USD (though it kinda dropped against safer currencies as people wanted those risk-on feels). 🌍

EUR kept flying higher during Thursday with dollar sagging, and U.S. jobless claims added more heat to the fire. By Friday, EUR walked away the second-best performer, getting those extra points from ECB’s potential moves vs. the slightly wishy-washy U.S. Fed standing. 🏆

Bullish Headline Arguments

- ECB members hinted at steady rates in the near term

- On Wednesday, ECB President Lagarde was all like, the euro scene’s holding up better than expected, and she thinks growth might just be on the up next week; she even said the money vibe is in a “good place” 🌟

- Lithuanian central bank boss Gediminas Simkus dropped some vibes saying there’s zero reason to slash rates since activity and price levels surprised us on the up⬆️

- ECB member Kazimir is like nah, let’s not tinker with rates in the upcoming months, “Absolutely not in December” 🚫

- ECB Governing Council mate Francois Villeroy de Galhau was clear on Wednesday that jacking up interest rates super soon isn’t on the menu. 🍽️

- Germany Industrial Production for October 2025: 1.8% m/m (0.4% m/m forecast; 1.3% m/m previous)

- Eurozone Sentix investor confidence for December: -6.2 (-6.2 forecast, -7.4 previous)

-

Germany Balance of Trade for October 2025: 16.9B (15.9B forecast; 15.3B previous)

- Germany Imports for October 2025: -1.2% m/m (0.5% m/m forecast; 3.1% m/m previous)

- Germany Exports for October 2025: 0.1% m/m (0.9% m/m forecast; 1.4% m/m previous)

Bearish Headline Arguments

- During his state visit to China, French Prez Emmanuel Macron dropped the tariff hammer on Beijing ✈️

- European Commission honcho von der Leyen clapping back at Trump: Don’t mess with European democracy 😒

- Over the weekend, ECB dude Rehn said the Euro area has downside feels medium-term, though prices are sitting at ECB’s 2% sweet spot 📉

- Germany Inflation Rate Final for November 2025: -0.2% m/m(-0.2% m/m forecast; 0.3% m/m previous); 2.3% y/y (2.3% y/y forecast; 2.3% y/y previous)

- France Inflation Rate Final for November 2025: 0.9% y/y (0.9% y/y forecast; 0.9% y/y previous)

GBP Pairs

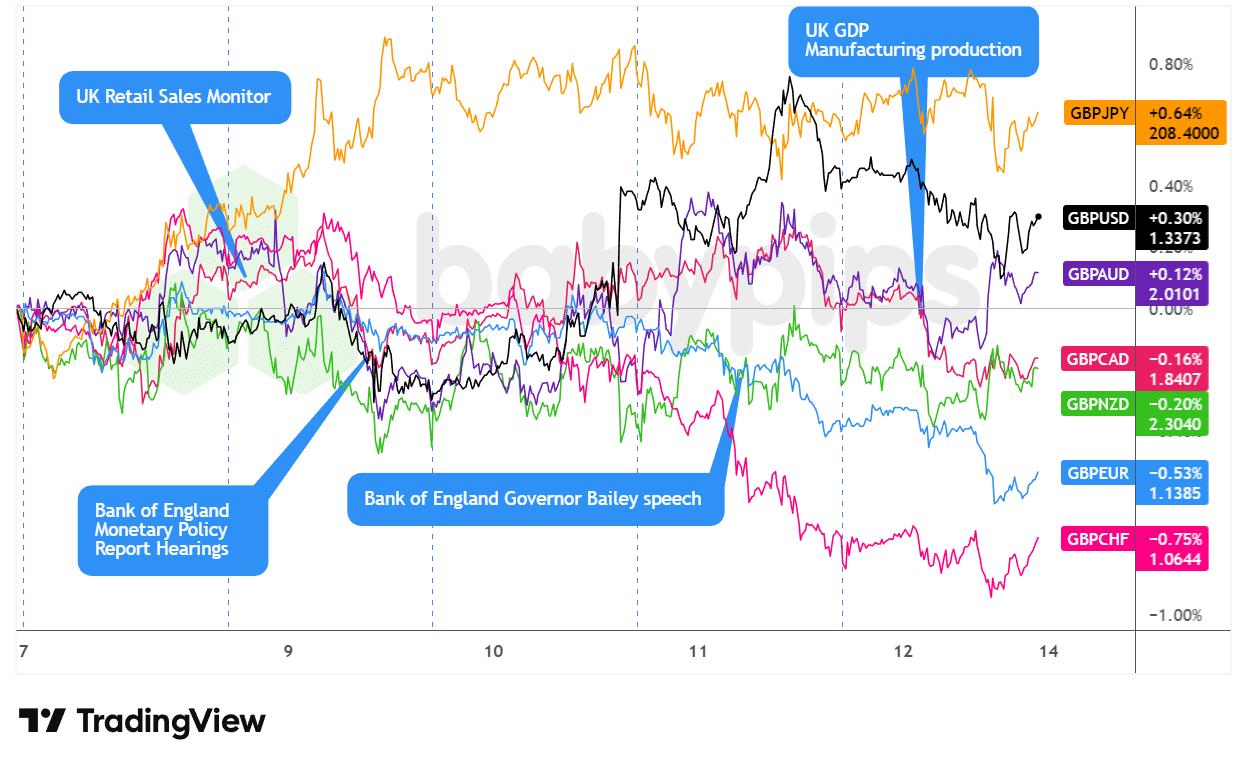

Overlay of GBP vs. Major Currencies Chart by TradingView

Sterling was treading water for most of the week until it hit an iceberg with low UK growth data. 🥶

The pound was in a traffic jam through Monday’s Asian and European sessions, feeling the weight when BOE's Taylor dropped a cautionary “bit on the brake” vibe, reminding that UK peeps ain't rushing for rate cuts. ⏳ This chill extended into Tuesday with meh UK BRC retail feels (1.2% y/y vs 1.5% before) pulling GBP back and probably leading to the late Tuesday slide.

Things got spicy on Wednesday with the Fed’s move. Powell’s chill take on tariff-driven inflation lifted rate-exposed currencies like the pound. Thursday was quieter, though Governor Bailey’s promise to shrink the bank’s stash might have provided minimal support, especially as GBP mixed things up, growing against USD and resource-based currencies but shrinking next to safe assets.

Friday wasn’t sweet, though. London time saw October GDP shrinking 0.1% month-to-month for back-to-back drownings, and services fell 0.3%—uncertainty about the budget still keeping us on edge. Markets quickly dialed up those rate drop expectations for the December 18th BOE meet-up, shoving the pound down to worst performer of the day. 📉

Bullish Headline Arguments

- BOE peeps want to take the cautious route with rate drops

- BOE’s Ramsden likes the “gradual ease-off of policy grip” approach, feeling it’s just right 🌬️

- BOE’s Lombardelli underscored the “upsides lurking in prices” while pushing for a careful route to rate-dropping

- BOE’s Dhingra sees disinflation being on track and no “mad rush for tense moves.”

- BOE’s Mann is doubtful that headline CPI will drop back to the golden target by mid-2027

- RICS U.K. House Price Balance for November 2025: -16.0% (-20.0% forecast; -19.0% previous)

- U.K. Manufacturing Production for October 2025: 0.5% m/m (0.5% m/m forecast; -1.7% m/m previous); -0.8% y/y (-1.2% y/y forecast; -2.2% y/y previous)

Bearish Headline Arguments

- BOE’s Taylor thinks inflation will hit the target “pretty soon” 📉

- UK BRC retail vibes for November: 1.2% y/y (2.5% forecast, 1.5% previous)

- The Financial Times spilled that the UK put up $2 billion extra on NHS to steer away from Trump’s tariff game

-

UK GDP for October 2025: -0.1% m/m (0.0% m/m forecast; -0.1% m/m previous); 1.1% y/y (0.9% y/y forecast; 1.1% y/y previous)

- UK Industrial Production for October 2025: -0.8% y/y (-0.9% y/y forecast; -2.5% y/y previous); 1.1% m/m (0.8% m/m forecast; -2.0% m/m previous)

- UK Goods Trade Balance for October 2025: -22.54B (-19.0B forecast; -18.88B previous)

- UK Balance of Trade for October 2025: -4.82B (-1.9B forecast; -1.09B previous)

- U.K. NIESR Monthly GDP Tracker for November 2025: -0.1% (0.1% forecast; 0.0% previous)

CHF Pairs

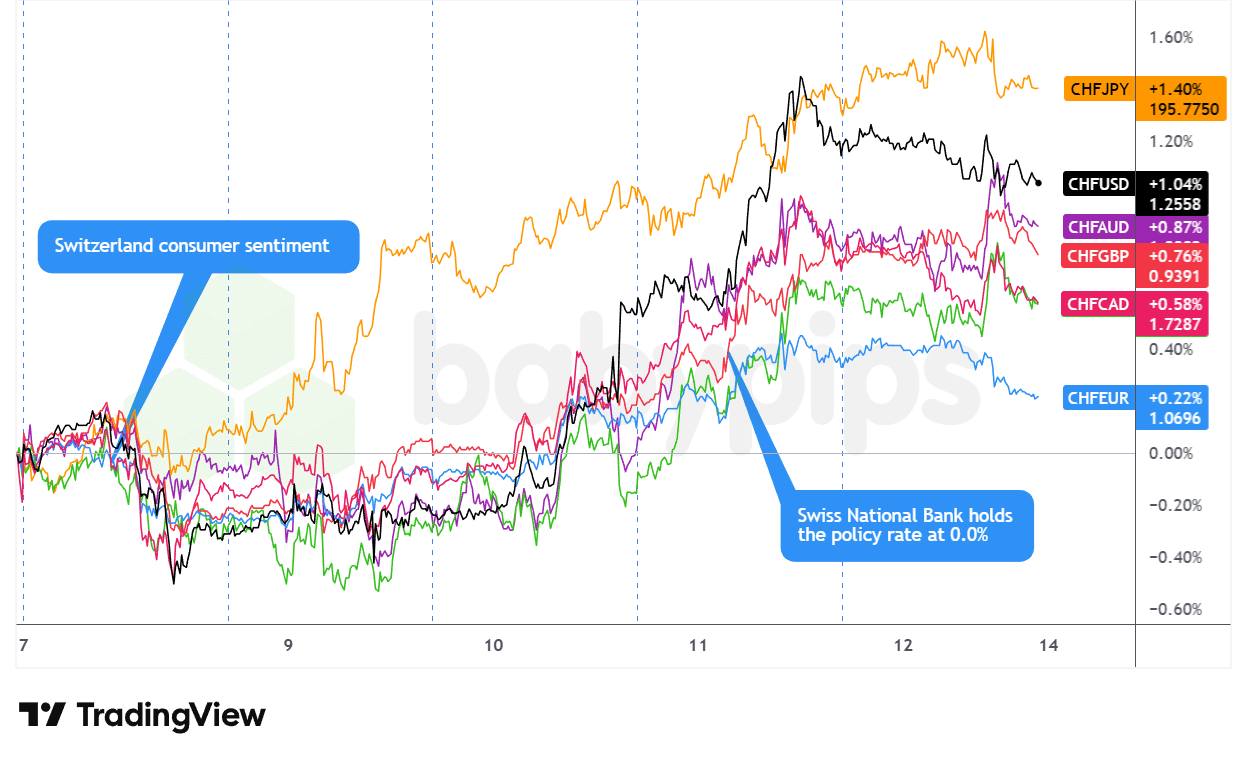

Overlay of CHF vs. Major Currencies Chart by TradingView

The Swiss franc slid through as the real boss currency this week, cruising from Monday to Thursday and then holding onto those gains until the party stopped Friday night. 🤙

Franc started off all over the place on Monday, gaining against currencies like Aussie and yen but getting dunked on by the euro, sterling, and good ol’ dollar as defensiveness was in vogue before the Fed call. Consumer vibes at -34.0 was meh, and even as Treasury yields crept up, the franc pulled a nosedive.

Tuesday dropped the Franc on a swag trail, gaining clout as folks nabbed Swiss assets for safe-squidgy feels leading up to FOMC night. 🚀 The rally exploded further on Wednesday when Fed went 25-bps cut and Chair Powell’s soft words made the dollar weep and moved CHF high on those charts. 💹

Thursday came with SNB’s call and no negative rates held firm despite weaker inflation calls, showing everybody easing wasn’t on their agenda. As jobless claims in the U.S. sagged, USD was thrown around, giving CHF more firepower till week's end. 🔥

Friday’s see-saw ended on a positive note, with risk-averse FOMO moves during tech slumps giving Swissy an extra pow. 📉

Bullish Headline Arguments

- Swiss Consumer Confidence for November 2025: -34.0 (-35.0 forecast; -37.0 previous)

- Swiss gov spilling tea on 15% US tariff max being backdated to mid-Nov. 📅

-

SNB Steady Against Negative Rates Although Inflation’s Softening, CHF Increases

- Swiss SNB Interest Rate Decision for December 11, 2025: 0.0% (0.0% forecast; 0.0% previous); feeling like the softer inflation calls aren’t enough to turn negative

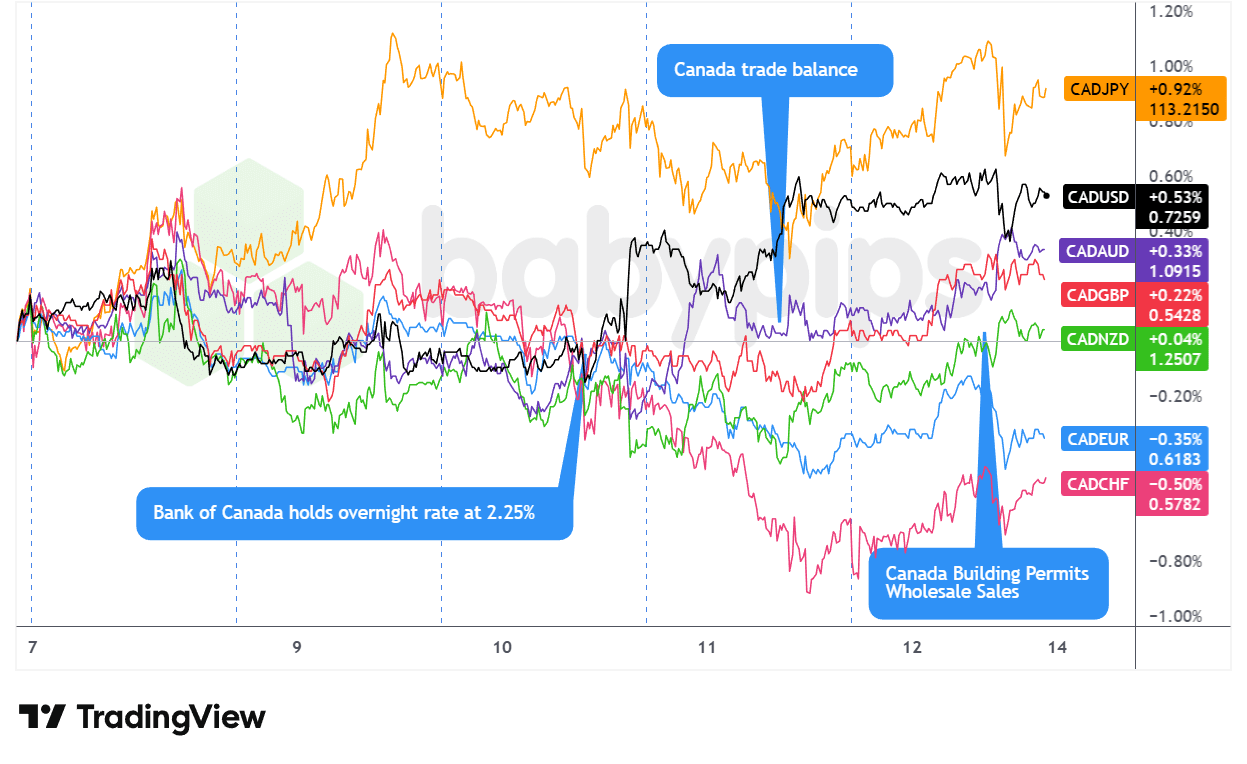

CAD Pairs

Overlay of CAD vs. Major Currencies Chart by TradingView

The Loonie hopped into this week on wobbly paws, dropping the previous week’s job hype under the crushing weight of sad oil prices and nervous minds ahead of central bank whispers, keeping the currency on its toes through Monday’s European and U.S. timezones. WTI’s dive and an increase in dollar fandom sparked proto-CAD grief through the week’s official open.

With the Fed and Bank of Canada ready to drop some lyrics, the Loonie fluttered through Tuesday and Wednesday, getting a boost from the hardy JOLTS story during the Tuesday U.S. sundown but then losing steam. Bank of Canada’s predictable no-change 2.25% call on Wednesday arvo was a key move—not the rate itself, but Governor Macklem’s sneak peek into the “neutral range” and hesitancy towards no future drops dropped consumer confidence a notch, even as later Fed chatter lightened the mood a bit.

Thursday U.S. showtime marked a twist as the weaker-than-expected jobless scenario (236K vs. the 205K call) punished the dollar, maybe adding some CAD color, especially compared to other currency outfits. Staying positive to Friday’s main theater, the Loonie finished not too faded, with a possibly bullish aura as bouncing commodity names—particularly in copper’s record spree—and soft dollar action helped shake off domestic missteps on wholesale tunes and ability jams. 💪

Bullish Headline Arguments

-

Canada Balance of Trade for September 2025: 0.15B (-6.0B forecast; -6.32B previous)

- Canada Imports for September 2025: 64.08B (67.0B forecast; 66.91B previous)

- Canada Exports for September 2025: 64.23B (61.0B forecast; 60.58B previous)

- Canada Building Permits for October 2025: 14.9% m/m (0.3% m/m forecast; 4.5% m/m previous)

Bearish Headline Arguments

-

BOC Holds at 2.25% As Canadian Economy Shows Resilience Despite Trade Uncertainty

- Canada BoC Interest Rate Decision for December 10, 2025: 2.25% (2.25% forecast; 2.25% previous)

- BOC members viewed the current interest range as a decent fit for the lower end in anchoring structural shift ⏳

- Canada Wholesale Sales Final for October 2025: 0.1% m/m (0.3% m/m forecast; 0.6% m/m previous)

- Canada Capacity Utilization Rate for September 30, 2025: 78.5% (79.2% forecast; 79.3% previous)

- Canada New Motor Vehicle Sales for October 2025: 163.5k (169.0k forecast; 168.7k previous)

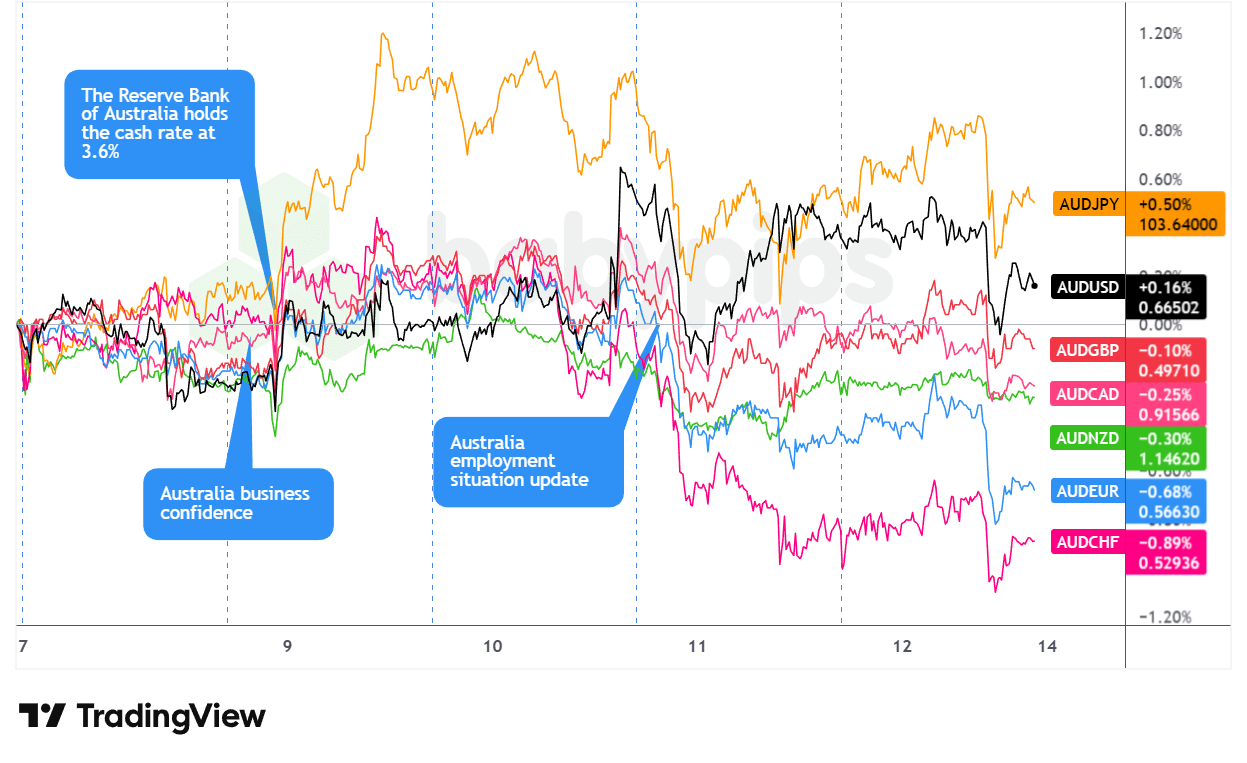

AUD Pairs

Overlay of AUD vs. Major Currencies Chart by TradingView

The Aussie chum opened the week on a lukewarm note, hitting mixed charts through Monday’s timezone action as gold prices steadied and folks gabbed nervously about major bank meet-ups. Even China flexing a $1 trillion trade score couldn't keep those defensive instincts at bay, damping any potential sparks before U.S. selling vibes took over.

Tuesday’s early hours dropped some turbulence for the Aussie. The RBA played nice with their 3.60% call as predicted, which nudged early sell-offs, but Gov Bullock’s hawkish noise chimed in on potential promising moves February, giving the Aussie a caffeine jolt, making it Tuesday’s superstar currency. 🌟

Momentum was fleeting as Wednesday’s Asian tune clashed with China’s underwhelming inflation tale—monthly CPI at -0.1% vs. the half-full +0.1%—unsettling the commodity darling heading to the Fed showdown. Thursday dealt a more intense blow as workforce numbers tanked by 21,300 vs. the 5,000 hopes, with participation rates slipping, leaving the Aussie trailing despite gold gliding up.

The week’s curtain calls with Friday’s tivvy-tavvy—Australian goodness held strong early in Asia before things derailed with tech flounders and fiery Fed lines pushing the yield compass north.

Bullish Headline Arguments

-

RBA Officially Keeps Rates Unchanged at 3.60%, AUD steps up bravely

- Australia RBA Interest Rate Decision for December 9, 2025: 3.6% (3.6% forecast; 3.6% previous) 📈

-

China Trade Balance for November 2025: 111.68B (92.0B forecast; 90.07B previous)

- China Balance of Trade (Yuan) for November 2025: 792.58B (640.49B previous)

- China Imports for November 2025: 1.9% y/y (2.5% y/y forecast; 1.0% y/y previous) 🚂

- China Exports for November 2025: 5.9% y/y (3.2% y/y forecast; -1.1% y/y previous) 🚢

- China Consumer Price Index Growth Rate for November 2025: -0.1% m/m (0.1% m/m forecast; 0.2% m/m previous); 0.7% y/y (0.6% y/y forecast; 0.2% y/y previous)

- US gives a nod and says "yes to Nvidia H200 chip sales to China", of course with that sweet 25% charge on each sale 💸

- China Total Social Financing for November 2025: 2,490.0B (1,650.0B forecast; 810.0B previous)

- China M2 Money Supply for November 2025: 8.0% (7.5% forecast; 8.2% previous)

- China Outstanding Loan Growth for November 2025: 6.4% y/y (6.3% y/y forecast; 6.5% y/y previous)

- China New Loans for November 2025: 390.0B (450.0B forecast; 220.0B previous)

Bearish Headline Arguments

- Slight jitters over China trade moves might limit AUD’s warm vibes

-

Australia’s Job Change Score for November 2025: -21.3k (5.0k forecast; 42.2k previous)

- Australia’s Unemployment Rate for November 2025: 4.3% (4.3% forecast; 4.3% previous)

- China Producer Prices Index change for November 2025: -2.2% y/y (-2.0% y/y forecast; -2.1% y/y previous)

- Australia Building Permits Final for October 2025: -1.8% y/y (-1.8% y/y forecast; 14.9% y/y previous)

- Australia Private Home Sign-Offs Final for October 2025: -2.1% (-2.1% forecast; 4.0% previous)

- Australia Development Approvals Final for October 2025: -6.4% (-6.4% forecast; 12.0% previous)

- Australia NAB Business Vibe Check for November 2025: 1.0 (6.0 previous)

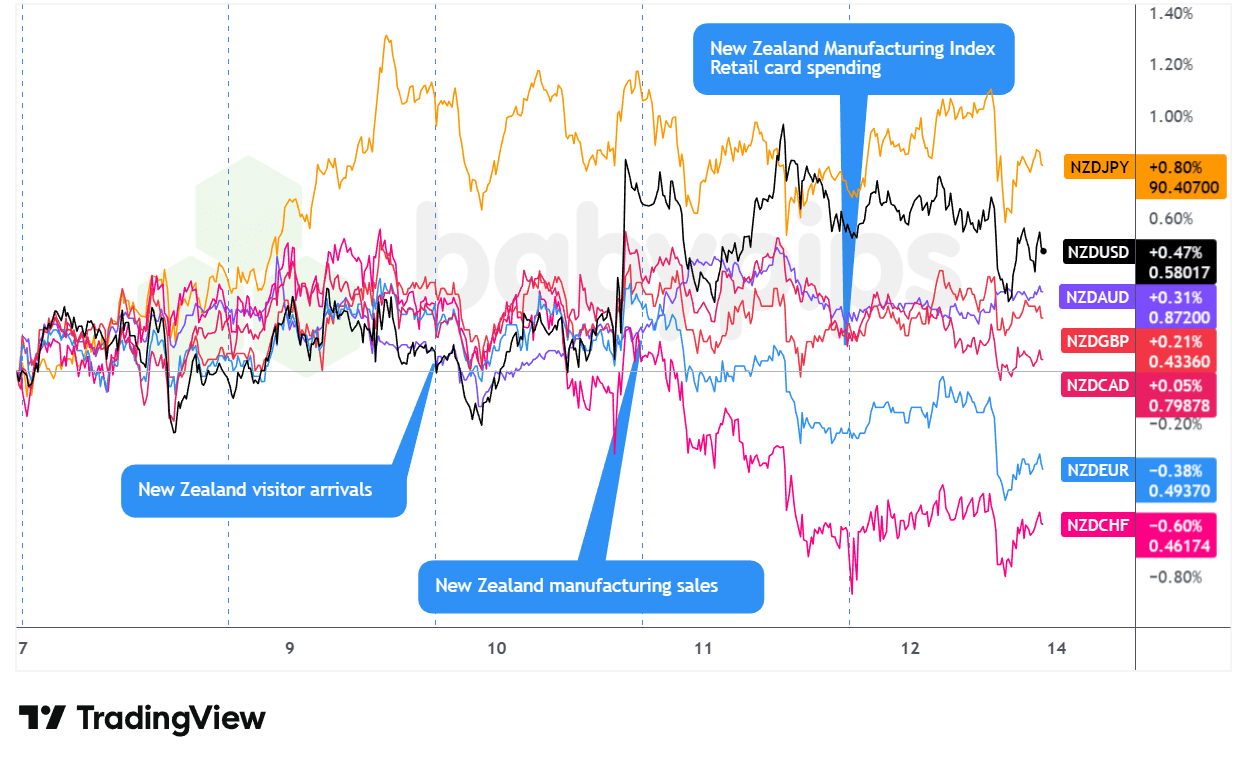

NZD Pairs

Overlay of NZD vs. Major Currencies Chart by TradingView

The kiwi slid into the week with its vibes pretty high, securing gains through Tuesday U.S. trading, thanks to China’s banging trade score during Monday Asia time and the RBNZ being less chill compared to the big leagues. The kiwi served alongside the Aussie's Tuesday surge after RBA Governor Bullock’s February inflation warning, before chilling through London.

Wednesday’s Asia time put some pressure as China’s softer inflation feels—CPI at -0.1% monthly versus 0.1% expected—hit the currency, but NZD picked up steam hopping into FOMC night. Powell’s soft speak on tariff-led inflation shot a late rally, pushing NZD against USD and commodity currencies, as it lagged behind European biggies.

The final bits went full grumpy bear. Thursday's U.S. session saw clear NZD dips linked to Australia’s unforgivable jobs show. Friday’s Asian bright spot from sweet domestic retail data flipped as AI stock woes and hawkish Fed talks sent mostly red flows through London and NYC stations. 📉

Bullish Headline Arguments

- New Zealand Passenger Arrivals for October 2025: 9.4% y/y (3.0% y/y forecast; 9.6% y/y previous)

- New Zealand Factory Sales for Q3 2025: 0.9% (-0.3% forecast; -0.6% previous)

- New Zealand Business NZ PMI for November 2025: 51.4 (50.5 forecast; 51.4 previous)

Bearish Headline Arguments

- RBNZ Chief Breman highlighted the lack of firm moves for policy vibes

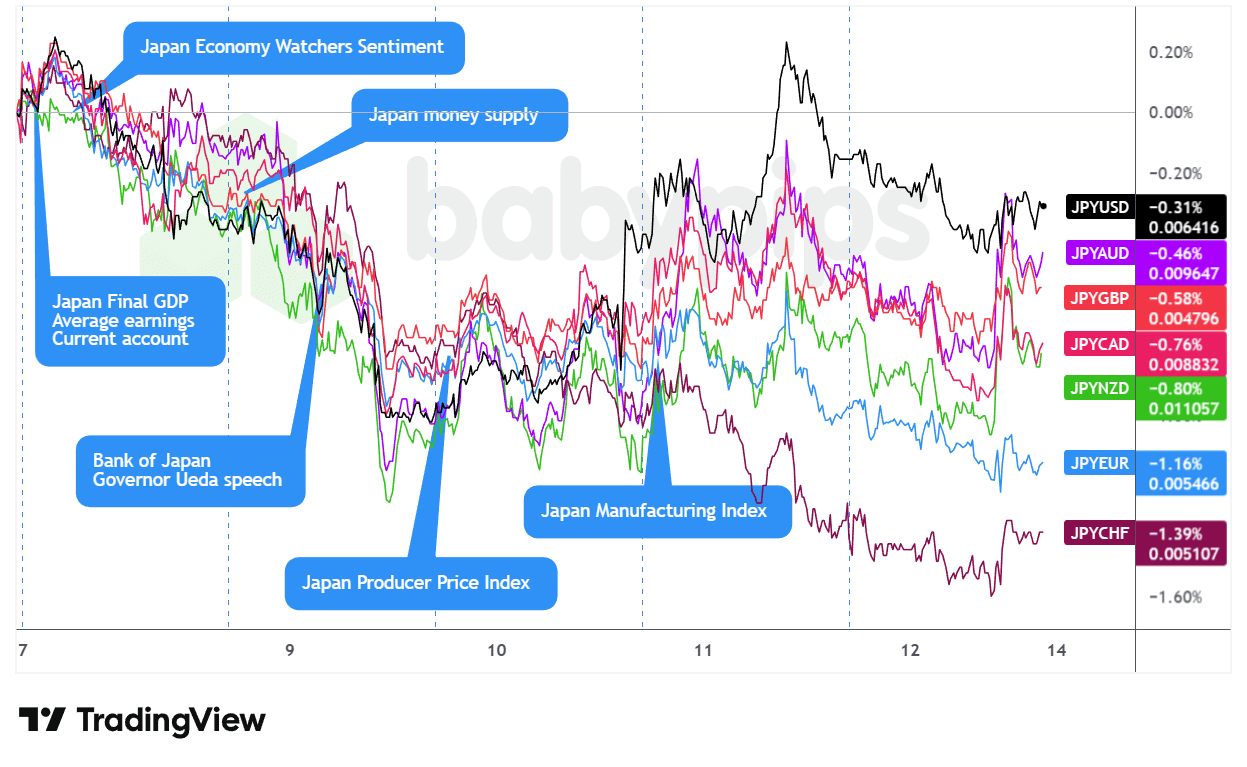

JPY Pairs

Overlay of JPY vs. Major Currencies Chart by TradingView

The yen started with existential feels—Finance Minister Katayama dropping a serious sigh about “one-sided, rapid moves,” yet lil' JPY slid during Monday's Asia sesh and kept rolling into Tuesday U.S. party. That's what’s up when markets already price in the expected BOJ upgrade coming the next week, leaving no room for redressing, while everyone else is tightening. 😬

Governor Ueda on Tuesday talking about quick rate hikes and bond purchasing tweakery didn’t help, leaving thoughts that BOJ wasn’t gonna do anything drastic, amping up the yen dip through London. The brokering session came the next day, an Asian session as China’s deflation tea spilled and safe-haven feely vibes took sway, though the safety was temporary as FOMC realignments yanked during London time. 💪

The yen had some glory Thursday U.S. opening with a swift comeback after a surprise jobless report dropped Treasury yields, but equity goodness erased those safety gains before wrapping up. The currency sauntered off into the night by sliding through Asia and European hours as the crazy rate differences came to play, with a tiny highlight during U.S. equity hours due to tech instability bringing little temporary sunshine. Soooooo JPY ended as the lowest major currency this past week, catching on the hawkish vibes already pried. 😅

Bullish Headline Arguments

- Japan’s Finance Boss Satsuki Katayama called out the yen’s wild “one-sided, rapid moves” 🎢

-

Japan Average Cash Earnings for October 2025: 2.6% y/y (2.1% y/y forecast; 1.9% y/y previous)

- Japan Overtime Pay for October 2025: 1.5% y/y (0.3% y/y forecast; 0.6% y/y previous)

- Japan’s Banking Vibe Lending for November 2025: 4.2% (4.1% previous)

-

Japan Final GDP Growth for Q3 2025: -0.6% q/q (-0.4% q/q forecast; 0.5% q/q previous)

- Japan GDP Price Index Final for Q3 2025: 3.4% (2.8% forecast; 3.0% y/y previous)

- Japan GDP Private Consumption Final for Q3 2025: 0.2% q/q (0.1% q/q forecast; 0.4% q/q previous)

- Japan’s Eco Watchers Survey Outlook for November 2025: 50.3 (49.3 forecast; 53.1 previous) 🕶️

- Japan’s Machine Tinker Orders for November 2025: 14.2% y/y (9.4% y/y forecast; 16.8% y/y previous)

- Japan PPI for November 2025: 0.3% m/m (0.2% m/m forecast; 0.4% m/m previous); 2.7% y/y (2.6% y/y forecast; 2.7% y/y previous)

- Japan BSI Large Manufacturing for Q4 2025: 4.7% (1.0% forecast; 3.8% previous)

- Japan’s Capacity Use Rate for October 2025: 3.3% (0.5% forecast; 2.5% previous)

Bearish Headline Arguments

- BOJ Governor Ueda shouted that long-term interest upticks are getting “somewhat breathless” 🚮

- Japan’s Reuters Tankan Index for December 2025: 10.0 (12.0 forecast; 17.0 previous)

- Japan GDP Growth Annualized Final for Q3 2025: -2.3% (-1.8% forecast; 2.2% previous)

- Japan GDP Capital Spend Final for Q3 2025: -0.2% q/q (1.0% q/q forecast; 0.8% q/q previous)

- Japan GDP Trade Ally Demand Final for Sept. 2025: -0.2% q/q (-0.2% q/q forecast; 0.2% q/q previous)

- Japan Trade Book for October 2025: 2,834.0B (2,900.0B forecast; 4,483.0B previous)

- Russian bombers linked with Chinese fly-patrol near Japan as Tokyo-Beijing beef peaks ✈️

- US and Japan vibe check through flight drills as China ramps military plans in Japan's airspace🎇

- Japan Industrial Output Final for October 2025: 1.6% y/y (1.5% y/y forecast; 3.8% y/y previous); 1.5% m/m (1.4% forecast; 2.6% previous)

Back to Table of Contents

This epic recap is for VIP use only on Babypips.com and don't even think about sharing it elsewhere without permission. 🤫✨